Latest from the Blog

In-depth guides on early retirement strategies, tax-efficient withdrawals, and making the most of your retirement accounts.

HSA vs FSA: Which Account Actually Wins in Retirement?

Most people in their 50s treat the annual benefits enrollment period as a chore. You check the boxes, keep the same health plan you had last year, and try to remember if you spent all the money in your Flexible Spending Account (FSA) before the deadline.

PenaltyFreeRetire Editorial · May 24, 2026

What Are Required Minimum Distributions — and How to Delay or Reduce Them

Required minimum distributions start at 73 for most traditional retirement accounts. Here is how RMDs work, why they raise taxes and Medicare costs, and what you can still do before they hit.

PenaltyFreeRetire Editorial · May 17, 2026

Roth IRA vs Traditional IRA: the decision that could cost (or save) you thousands

If you want to see how conversions would work with your actual numbers — your age, your balance, your income trajectory — the Roth Conversion Ladder Planner runs the year-by-year tax math for you. It shows where each conversion amount lands in the brackets, what your RMDs will lo

PenaltyFreeRetire Editorial · May 9, 2026

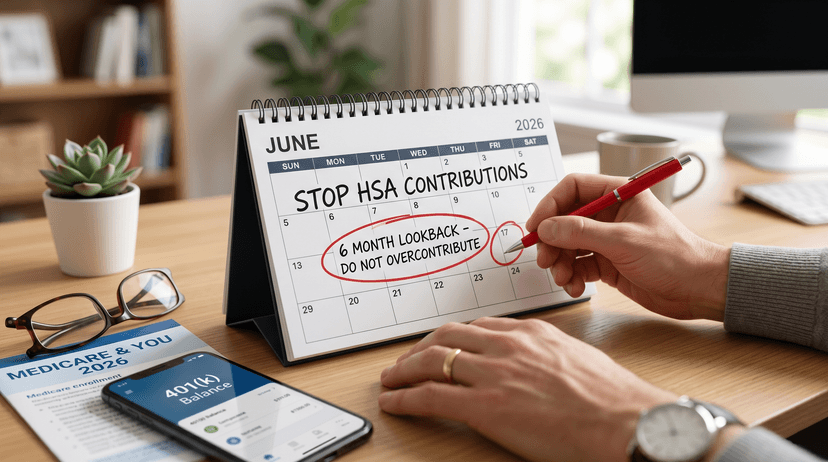

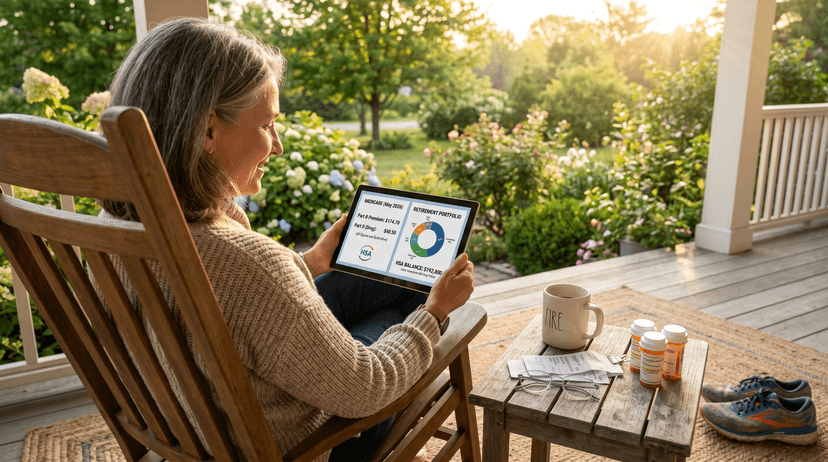

What Happens to Your HSA at 65 — and Why It Changes Everything

Most people stop paying attention to their HSA around the time they think about retiring. That is the wrong move. At 65 the rules flip in your favor, and the HSA becomes the most tax-efficient account you own. The same birthday introduces a Medicare timing problem that can quietl

PenaltyFreeRetire Editorial · May 2, 2026

Roth Conversion vs. Roth Contribution: Which Strategy Wins If Tax Rates Rise?

Is it better to contribute or convert? Contributions face strict IRS caps, but conversions let you move unlimited pre-tax wealth into Roth space. If tax rates rise, conversions win bigger for large balances by locking in today’s rates on more of your money before they climb.

PenaltyFreeRetire Editorial · May 2, 2026

Don't Roll Over That 401(k): The Early Retirement Mistake That Costs Thousands

Standard advice says roll your 401(k) into an IRA, but for early retirees, it can be a **costly trap**. The **Rule of 55** keeps your cash penalty-free—but only if it stays in the plan. Don't lock your money behind a 10% wall just when you’re breaking free.

PenaltyFreeRetire Editorial · May 2, 2026

Pay Now or Invest? When to Actually Spend Your HSA

Stop treating your HSA like a medical debit card—it's the most expensive way to use it. Instead, pay out of pocket and save receipts; let that balance compound tax-free for decades. It’s a triple-tax win that turns a $2,000 bill into a $7,700+ retirement asset.

PenaltyFreeRetire Editorial · May 2, 2026

Rule of 55 vs. 72(t) SEPP: Which Early Retirement Strategy Is Right for You?

Stop handing the IRS a 10% tip on your early retirement. Whether you need the flexible Rule of 55 or the rigid "lock-in" of SEPP 72(t) depends on your age and account types. Pick the right escape hatch now or pay for it—literally—until you're 59½.

PenaltyFreeRetire Editorial · May 2, 2026

The Rule of 55 Explained: Tap Your 401(k) Early Without the 10% Penalty

Think you’re stuck waiting until age 59½ to access your retirement savings? Think again. The Rule of 55 is a powerful, legal exception that allows early retirees to tap into their 401(k) without the dreaded 10% penalty—but most people disqualify themselves before they even start.

PenaltyFreeRetire Editorial · May 1, 2026

The HSA Stealth IRA: Why Your Health Savings Account Is the Best Retirement Account You're Ignoring

Most people treat their HSA like a medical debit card -- money goes in, receipts get paid, balance stays near zero. That's a mistake. An HSA is a retirement account with better tax treatment than any IRA or 401(k) on the market. It just happens to have "health" in the name.

PenaltyFreeRetire Editorial · May 1, 2026

The Roth Conversion Sweet Spot: How to Find Your Optimal Annual Conversion Amount

Your optimal conversion amount is the gap between your taxable income and the ceiling of your current tax bracket — your "bracket headroom." The PenaltyFreeRetire Roth Conversion Ladder calculator figures this out for you.

PenaltyFreeRetire Editorial · May 1, 2026

Why the First Five Years of Early Retirement Can Make or Break Your Roth Ladder

The Roth conversion ladder fails in year one if you don't have a bridge. You need five years of already-seasoned Roth contributions, or another source of cash, before your first converted dollar becomes accessible. Miss that and you're either paying a 10% early withdrawal penalty

PenaltyFreeRetire Editorial · May 1, 2026